Respa Gift Limits

Respa Gift Limits - James Chen, CMT, is an expert trader, investment advisor and global market strategist. The Real Estate Settlement Procedures Act (RESPA) was enacted by the US Congress in 1975 to provide buyers and sellers with full information about settlement costs. RESPA was also enacted to eliminate unfair practices in the estate settlement process, prohibit kickbacks, and limit the use of escrow accounts.

Source: m.media-amazon.com

Source: m.media-amazon.com

Respa Gift Limits

RESPA is a federal law currently regulated by the Consumer Financial Protection Bureau (CFPB). Originally enacted by Congress in 1974, RESPA became effective on June 20, 1975. RESPA has been amended and supplemented over the years. Enforcement originally fell under the jurisdiction of the US Department of Housing and Urban Development (HUD).

After 2011, these responsibilities were assumed by the CFPB under the Dodd-Frank Wall Street Reform and Consumer Protection Act. Since its inception, RESPA has regulated mortgage loans related to one- to four-family residential properties. The purpose of RESPA is to inform borrowers of their settlement costs and eliminate kickbacks and brokerage fee practices that can increase the cost of obtaining a mortgage.

The types of loans covered by RESPA include most home equity lines of credit, foreclosures, refinances, home improvement loans, and home equity lines of credit (HELOCs). RESPA does not apply to loans to the government, government agencies or instrumentalities, or in situations where the borrower plans to use the property or land primarily for business, commercial, or agricultural purposes.

What Is The Real Estate Settlement Procedures Act (Respa)?

RESPA requires lenders, mortgage brokers, or home loan servicers to provide borrowers with any information about real estate transactions. Disclosures should include settlement services, applicable consumer protection laws, and any other information related to the costs of the estate settlement process. Business relationships between closing service providers and other parties involved in the settlement process must also be disclosed to the borrower.

Source: image.slidesharecdn.com

Source: image.slidesharecdn.com

RESPA prohibits certain practices such as kickbacks, referrals, and unearned fees. For example, Section 8 prohibits any person from giving or receiving anything of value in exchange for a settlement business recommendation. It also regulates the use of escrow accounts — for example, prohibiting lenders from requiring excessively large escrow accounts — and restricts sellers from ordering insurance companies.

RESPA allows an exception where brokers and agents may exchange reasonable payments in exchange for goods or services provided by other clearing service providers, provided the arrangements comply with law and regulatory guidance. RESPA does not prohibit joint marketing efforts between a realtor and a lender as long as the advertising expenses paid by each party are related to the value of any goods or services that may be received in return.

However, transactions in which one party pays more than a pro rata share of ad spend are prohibited. Event sponsorship may also be prohibited if one party uses the event to sell or advertise their services. Real estate agents and brokers are prohibited from entering into contracts for marketing services where one party charges the other for marketing materials an amount that exceeds the fair market value of the marketing services rendered.

Understanding The Real Estate Settlement Procedures Act (Respa)

A settlement service provider may not rent space from another settlement service provider unless it pays fair market value for it. Realtors cannot pay agents to refer clients to a mortgage broker's affiliate. Brokers may not offer fees to other brokers for referring clients to their business.

These co-op fees are prohibited and are essentially considered a form of kickback. Mortgage lenders cannot offer any incentives to local real estate agents for referring home buyers to their loan products. Realtors cannot refer business to an affiliated title company without disclosing the relationship to their clients.

Source: eadn-wc03-6532417.nxedge.io

Source: eadn-wc03-6532417.nxedge.io

This disclosure should include details of the fees the title company charges for its services and the broker's financial interest in the title company. Customers should also be aware that they are under no obligation to use the title company they were referred to. Real estate agents and insurance companies cannot set up affiliates to collect referral dividends.

Lenders cannot require borrowers to use a specific settlement service provider partner. However, they can provide financial incentives to do so. For example, a home buyer may be able to use partner services at a reduced rate. A plaintiff has up to one year to file suit to enforce kickbacks or other violations in the settlement process.

Respa Requirements

If a borrower has a claim against their loan servicer, they must take certain steps before filing a lawsuit. The borrower must contact his lender in writing detailing the nature of his problem. The administrator is obliged to respond in writing to the debtor's complaint within 20 working days from the moment of receipt of the complaint.

The administrator has 60 business days to resolve the issue or provide reasons for the current account status. Borrowers must continue to make the required payments until the problem is resolved. If you are not using an attorney during a real estate transaction, it is best to contact them immediately if you believe a RESPA violation has occurred.

A real estate lawyer can help you navigate the legal process. An applicant has up to three years to file a claim for certain deficiencies against their credit servicer. Any of these actions may be brought in any federal district court in the district where the property is located or the alleged violation of RESPA occurred.

Source: static01.nyt.com

Source: static01.nyt.com

Critics of RESPA say some of the unfair practices the law is supposed to eliminate, including kickbacks, still occur. One example is lenders who provide their own liability insurance to the insurance companies they work with. (The insurance company is a wholly owned subsidiary of a larger firm whose job is to write insurance policies for the parent company, not to insure another company.) Critics say this is essentially a kickback mechanism because customers usually

What Does Respa Prohibit?

choose the services of suppliers. who are already connected to their lender or estate agent (although customers must sign documents stating that they are free to choose any service provider). Because of these criticisms, there have been many attempts to change RESPA. One of the proposals includes removing the ability for customers to choose any provider for each service.

Instead, there would be a system where the services are bundled, but the real estate agent or lender is directly responsible for all other costs. The advantage of this system is that lenders (who always have more purchasing power) will be forced to seek the lowest prices of all real estate settlement services.

The Real Estate Settlement Procedures Act (RESPA) is designed to protect consumers who want to get a mortgage loan. However, RESPA does not protect all types of loans. Loans secured against real estate for commercial or agricultural purposes are not covered by RESPA. RESPA requires borrowers to obtain different information at different times.

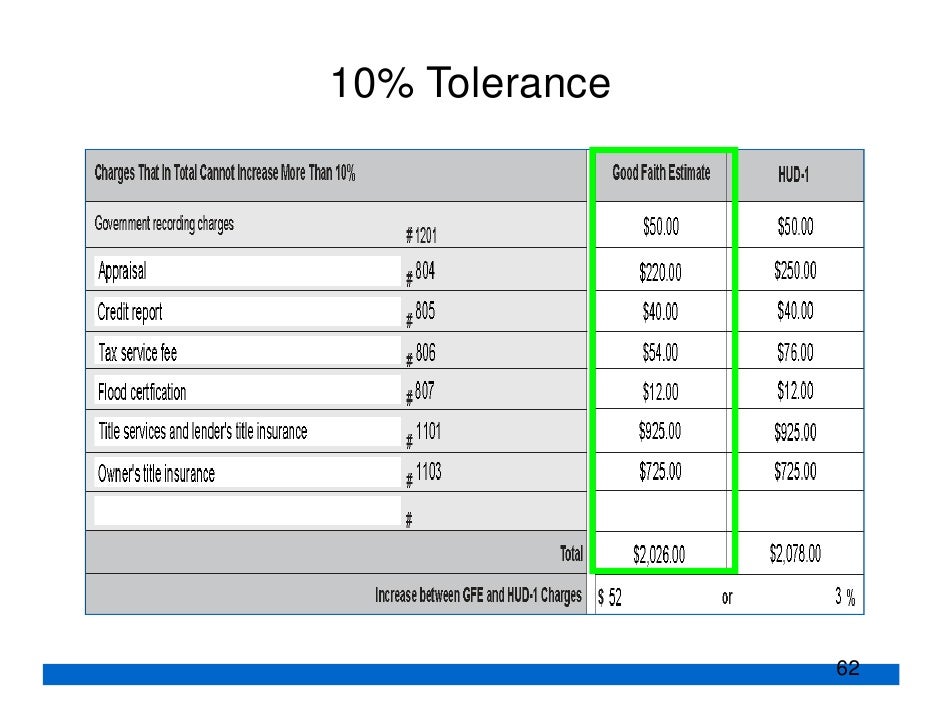

First, the lender or mortgage broker should give you an estimate of the total settlement fees you're likely to have to pay. (This estimate is a good faith estimate; however, actual costs may vary.) The lender or mortgage broker must also provide a written statement when you apply for the loan, or within three business days if they expect someone else to take over the mortgage payments