Fha Gift Rules

Fha Gift Rules - Fannie Mae customers! Get answers to your marketing guide and policy questions with Fannie Mae's AI-powered search engine. A mortgage loan secured by a primary residence or second home can be used by the borrower as a personal gift from a qualifying donor. Funding may fund all or a portion of the down payment, closing costs or finance reserve subject to the borrower's minimum contribution requirements below.

Source: templatelab.com

Source: templatelab.com

Fha Gift Rules

Donations may not be made to invest in property. Note: Equity gifts cannot be used for financial reserves. For additional information, see B3-4.3-05, Gifts of Stock. Identified by a relative, spouse, child or other dependent of the borrower or other person related to the borrower by blood, marriage, adoption or legal guardian.

or an unrelated person who has a family relationship with the borrower, his or her domestic partner (or a relative of the domestic partner), an individual engaged in the borrower's marriage, a previous relative, or a parent. Donors must not be affiliated with founders, developers, builders, real estate agents, or other persons interested in the business.

Note: A donor of equity is not considered an interest in the transaction. For information on organizational grants (grants), see B3-4.3-06, Grants and Borrower Contributions. The table below outlines the minimum lender requirements for gift-related transactions. Borrowers must provide at least 5% of their own capital as a loan.

Gift Funds

1 After the borrower's minimum contribution is met, gifts can be offset against down payments, closing fees, and reserves. See B5-6-02, HomeReady Mortgage Underwriting Procedures and Requirements, for HomeReady mortgage borrower contribution and prepayment requirements. The gift must be confirmed by a letter signed by the donor.

Source: moreirateam.com

Source: moreirateam.com

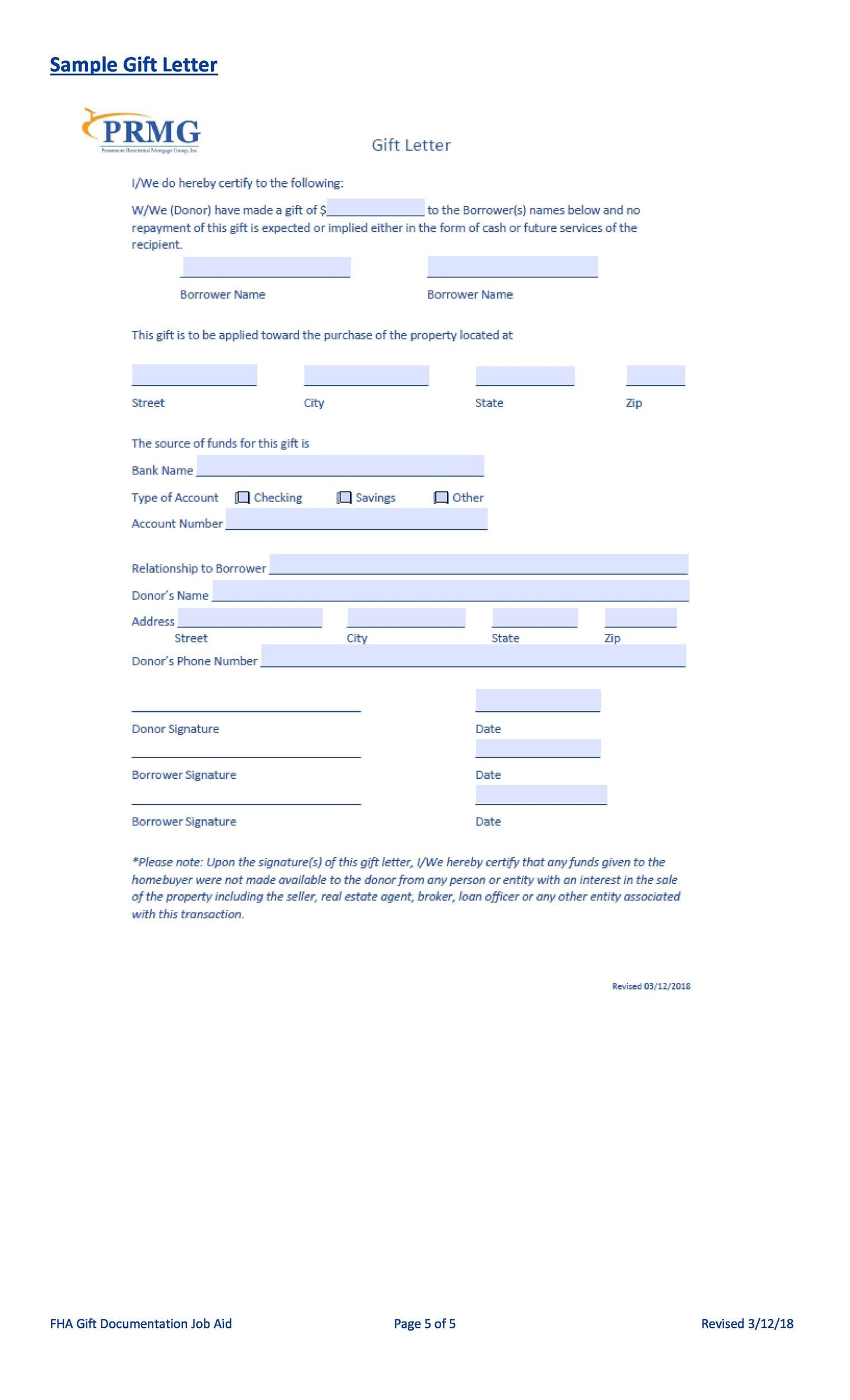

A gift letter must: Specify the actual or maximum dollar amount of the gift. Provide the donor's name, address, phone number, and relationship to the borrower. Note: If the actual amount of the gift received is different from the amount used to write the loan case file in DU, the borrower should send the loan case file to DU according to B3-2-10, DU data.

Accuracy, DU Tolerance, and Errors in Credit Reporting B3-2-10, Accuracy of DU Data, DU Tolerance, and Errors in Credit Reporting. For underwritten loans, the borrower must prove that the borrower has sufficient funds for closing, payment and/or financial reserves. When a qualifying donor's gift is combined with the borrower's funds to meet the required minimum down payment, it must also include the following items: Certification that the individual-donor has lived with the borrower for the past 12 years.

Months and does so in a new apartment. Documents showing the borrower's and lender's shared residential history. The address of the donor should be the same as the address of the borrower. For example, have a copy of your driver's license, receipt or bank statement.

Minimum Borrower Contribution Requirements

Borrowers must verify that there are sufficient funds in the donor's account (such as a checking, savings or investment account with the donor) or to transfer to the borrower's account. Relevant documents include: a copy of the donor's check and borrower's deposit slip, a copy of the donor's receipt and borrower's deposit slip, proof of electronic transfer of funds from the donor's account to the recipient's account, or a copy of the donor's check to the closing agent

When funds are not transferred to the closing agent or prior to eviction, the lender must document the donor's gift of funds to the closing agent in the form of a wire transfer, certified check, or cashier's check. Other official reviews. The table below shows recent publications related to this topic.

Source: i.pinimg.com

Source: i.pinimg.com

If a borrower receives a gift from a qualifying donor who has lived with the borrower in the past 12 months, is the gift considered the borrower's own money and can it be used to meet the lender's minimum contribution requirement when used by both individuals?

A house purchased as their primary residence. Ask Paul for exclusive FAQs and other official sales and service guide content. If you have additional questions, Fannie Mae customers can visit the Asking Pool for information from other published Fannie Mae sources. For a comprehensive list of resources such as access forms, notices, lender letters, and notices.

Documentation Requirements

If you're on the Galaxy Fold, consider opening your phone or viewing it in full screen mode to maximize your experience. Most home buyers need a down payment when buying a home. If someone gives you a portion of that money, it's called a prepayment gift.

You can use it to pay off any or all of your advance payments. There are rules about who can give a prepayment gift and how much the prepayment can be. Below, we'll cover all the details you need to know about prepaid gifts. A down payment gift is money given to a home buyer for a down payment.

There are strict rules for paying gifts. The rules vary depending on the type of loan. There are rules to ensure that the borrower gets home ownership. Your mortgage lender must prove that the money is a gift and not a loan. Otherwise, you (the borrower) will have an additional debt obligation—to repay the loan—which will affect your ability to make mortgage payments.

Source: www.credible.com

Source: www.credible.com

Prepaid gift rules cover two main areas: who can make a gift and how much can be prepaid. You also need to prove that the money is a gift and not a loan. Here's a rule of thumb for conventional loan payment offers: Most conventional mortgage lenders prefer 20% down.

Verifying Donor Availability Of Funds And Transfer Of Gift Funds

Buyers with less than 20% are usually required to purchase private mortgage insurance to protect their lenders. However, a 10% down payment is common. And some lenders even offer just 3% down. FHA mortgage down payment discount rules: FHA mortgages are guaranteed by the Federal Housing Administration.

If you have a credit score of 580 or higher, the minimum payment is 3.5%. If your credit score is between 500 and 580, you should put 10% down. FHA loans typically require mortgage insurance. VA lenders do not require a down payment or mortgage insurance.

If you receive a prepaid gift, you can take the money home with a small loan. Or the gift may go toward closing costs. USDA loans do not require a down payment if you meet certain income criteria. Note that a USDA loan will have a mortgage, which will increase your monthly payments.

As with VA loans, you can still receive a gift to pay closing costs or reduce your loan balance.

fha acceptable gift family members, fha gift limits, fha allowable gift donors, fha gift guidelines 4000.1, fha gift from cousin, gift of equity fha guidelines, fha gift funds 4000.1, fha gift letter pdf