Fha Gift Guidelines

Fha Gift Guidelines - RayID: 7bf1928dbb6d406d IP: 36.82.97.81 We've started a new series of blog posts that will answer the most frequently asked questions about FHA-insured mortgages. Today's question: Can an FHA down payment be gifted from a family member in 2017? The short answer is yes, the minimum down payment required for an FHA loan in 2019 (3.5%) can be provided from approved sources other than a family member, friend, employer or friend.

Source: www.pdffiller.com

Source: www.pdffiller.com

Fha Gift Guidelines

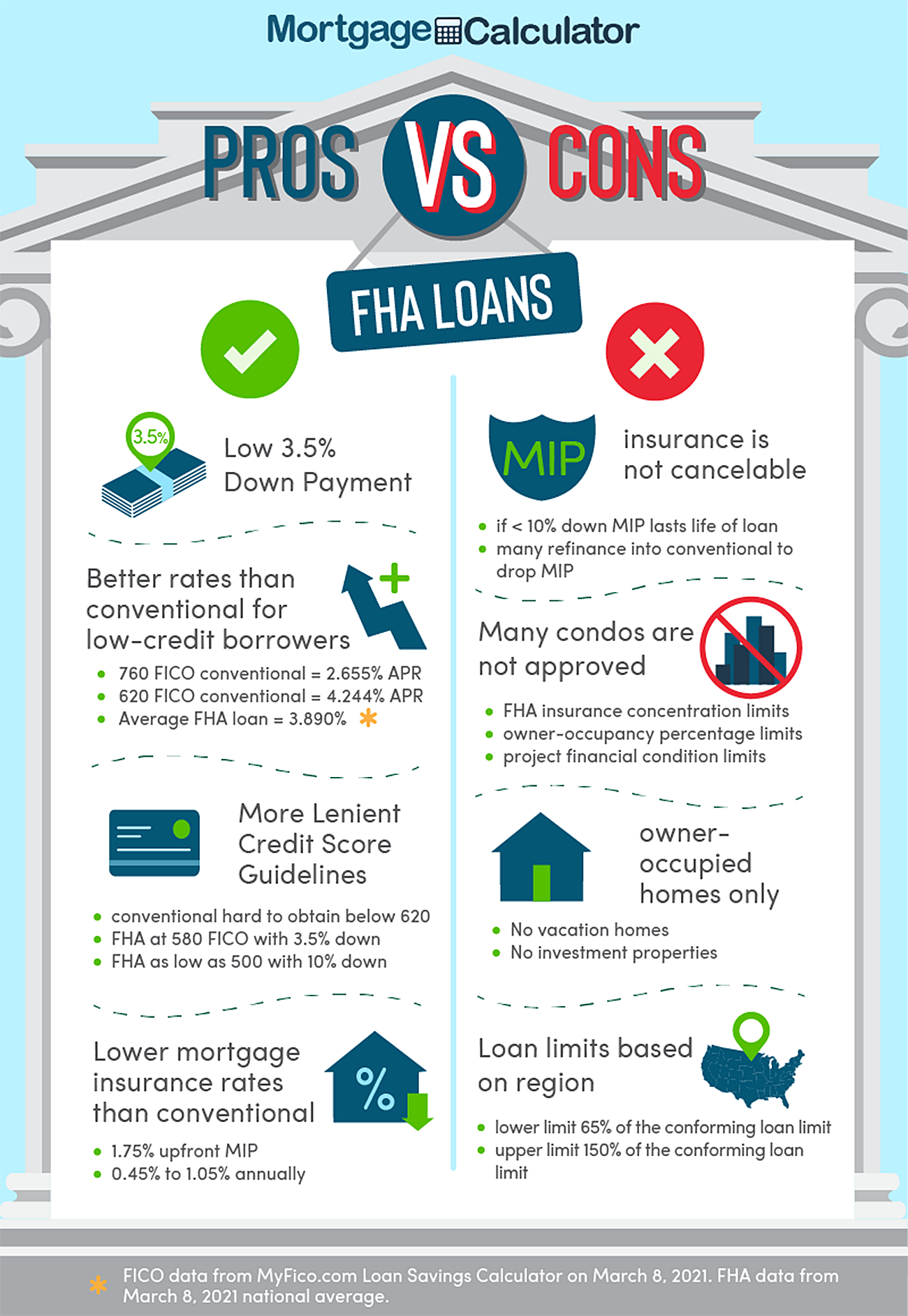

All of this is outlined in HUD Manual 400.1, Single Family Housing Policy Manual. With that simple answer in mind, let's take a closer look at the rules and procedures for FHA prepaid gifts. According to the Department of Housing and Urban Development, which administers the FHA loan program, borrowers must pay a minimum of 3.5% down when applying for the program.

Specifically, 3.5% of the home's purchase price or appraised value, whichever is lower. This very low fee is part of what attracted people to the program in the first place. The good news is that this upfront investment doesn't necessarily come out of the homeowner's pocket.

An FHA down payment can be provided from a family member or other approved sponsor, as determined by HUD guidelines and requirements for 2017. Part of the reason this program is so popular with low- and moderate-income borrowers (although it's certainly not limited to that).

Can My Fha Down Payment Be Gifted?

In the FHA's policy manual, HUD defines a gift as "a cash or stock contribution without expectation of income." The last four words are very important. If a family member, employer or other approved sponsor offers you money to pay off your mortgage, you are not expected to be paid.

Source: www.mortgagecalculator.org

Source: www.mortgagecalculator.org

In other words, the money being given should really be a gift, not a loan. You can have money loaned to you, but you can't borrow money from others. Per HUD Guide 400.1, FHA down payment gifts may be provided as follows: We understand that sellers may add funds to the buyer's closing costs, but not to the down payment.

HUD considers sellers, real estate agents, builders, and developers to be "parties interested in the transaction." These stakeholders do not have to contribute money to the borrower's minimum required investment, aka MRI. This is in accordance with HUD Handbook 4000.1 (page 232). So we've answered the main question: Can my FHA payment be gifted to a third party?

The answer is yes, as long as it is included in the list of approved donors above (and in the HUD manual). In 2017, there are additional requirements for FHA prepaid gifts. Mortgage lenders who finance the loan must obtain a "gift letter" from the lender.

Can My Fha Down Payment Be Gifted?

At the very least, this letter should state that the sponsor does not expect any form of compensation as described above. It should also reveal the nature of the relationship. If a third party owes you part or all of your down payment, the mortgage lender must properly document the transfer before closing.

It also has special requirements as detailed below. The following gift letter documentation requirements are found in HUD Handbook 4000.1: FHA prepaid gift funds are sometimes paid to the settlement agent. In such cases, the lender must confirm that the sponsor has received the donated funds.

Source: i.ytimg.com

Source: i.ytimg.com

Mortgage lenders must ensure that the funds are from an acceptable source as described above. If documentation from a bank or other savings account is not available, the lender "must require the donor to provide written proof of receipt of funds from an acceptable source and not from other parties to the transaction."

Again, this is all taken directly from the Family Housing Policy Manual (4000.1). If you have additional questions on this topic, please refer to the official policy manual for answers. Back to the current question: Yes, an FHA down payment can be obtained from a family member, friend, employer, etc.

No Expectation Of Repayment

can be gifted. - if you meet the above requirements and other gift rules and requirements set forth by HUD. By the way, FHA approved mortgage lenders must be aware of all of these requirements. So they can guide you through the process. Supporting Documents |

The right source Authorized Sponsors | Alternatives to prepaid support Summary | Frequently Asked Questions For FHA loans, homebuyers can receive 100% of the down payment or down payment as a financial gift. If the gift is not a loan and is not from someone who has a financial interest in the home, you can use the gift money to purchase a home.

Search: Find your agent with Smart Real Estate, save when you buy! An FHA gift fund is a property provided by a sponsor to help a homeowner close: No, gift funds do not have to be "seasonal." means that you should not be on your account at a certain time.

Source: gustancho.com

Source: gustancho.com

To verify that a gift fund is truly a gift, FHA lenders will ask you to provide two documents: a gift letter and a financial statement. wants to What documents you send depends on your situation: Donor money: In general, the FHA doesn't care where the donor money comes from, as long as you're not obligated to pay it back and the money doesn't come from someone who has an interest in the property.

No Expectation Of Repayment

Cash is not a reliable source of gift funds. If your sponsor gives you money, ask them to send you an electronic transfer or a check (may need a cashier's or certified copy). The FHA is also strict about who can give you gifts. Permissible sponsors include anyone who is interested in you but not interested in buying a home (they may not have a financial stake in the property).

If you don't receive a gift of security, you can get help with your down payment: A co-borrower pays a monthly mortgage - their first name and last name can live on the home. A co-signer refers to your loan-to-income relationship. A higher income will lower your DTI and can help you get a lower payment.

If you're buying your first home, you can apply for one of 2,500 down payment or down payment assistance and first-time home buyer loan programs across the United States. Yes, the FHA allows down payments and gift funds from donors who are interested in the borrower - such as family members, close friends, employers, charities and government agencies.

Yes, gift funds can be used for various home purchases. High cash reserves or emergency savings can help you qualify for FHA if you have a high debt-to-income ratio (DTI). In general, the FHA does not care where the donor's money comes from. If you are not obligated to pay them back and they do not come from a person interested in the property, your FHA lender will accept the gift money from your business account.

fha acceptable gift family members, fha gift guidelines donor, fha gift guidelines 4000.1, fha gift guidelines 2023, fha gift documentation guidelines, fha gift of equity guidelines, fha gift of equity guidelines 2022, fha gift of equity