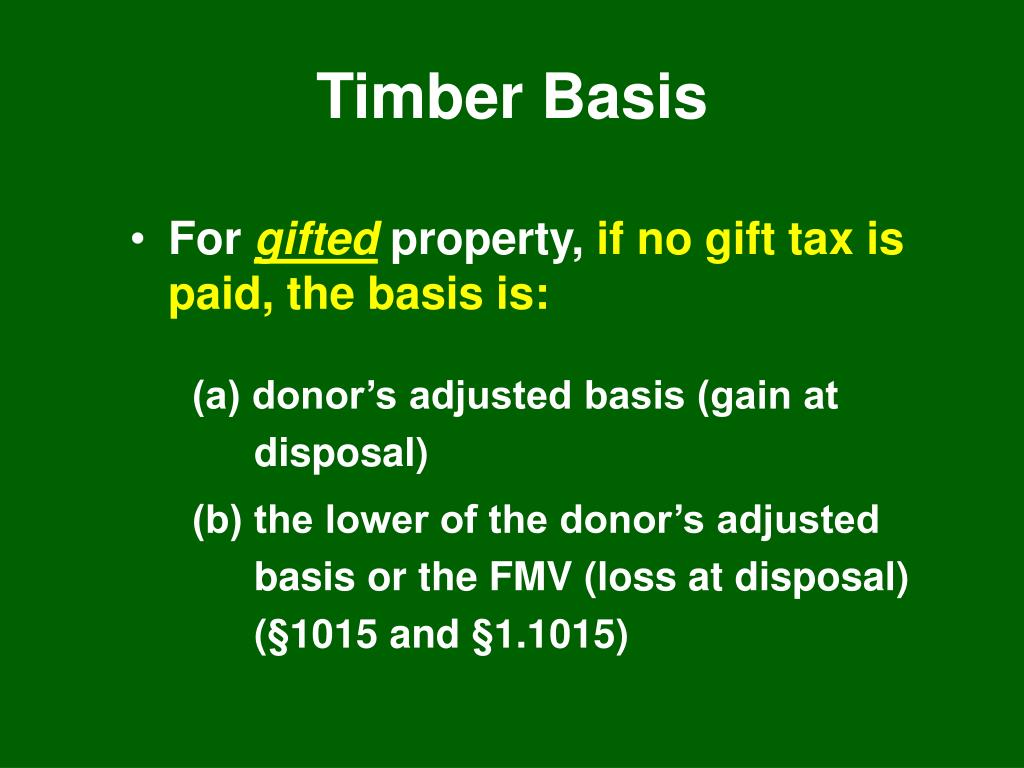

Donor's Adjusted Basis Of Gift

Donor's Adjusted Basis Of Gift - You may end up paying gift tax or capital gains tax. Transfers of property made before the death of the original owner are gifts, not legacies, and the tax code distinguishes between them. You may receive real estate or other assets as gifts, but you would prefer the cash value of the asset.

![]() Source: www.richlandcountyfoundation.org

Source: www.richlandcountyfoundation.org

Donor's Adjusted Basis Of Gift

Recipients of gifted property face different tax consequences than recipients of inherited property if they decide to sell. The Internal Revenue Service (IRS) does not consider donations to be income, even if they are in cash. Your rich grandma can give you a million dollars and you won't owe the taxman a dime.

You also won't owe the IRS gift tax if your grandmother gives you an in-kind gift. You will only have to pay this tax if you decide to donate or sell the gift for significantly less than its market value. In tax year 2022, you could give $16,000 a year in cash or property to anyone without paying gift tax.

The limit has increased to $17,000 for 2023. If you donate more, it will apply to your lifetime exemption. The lifetime exemption is $12.06 million for 2022 and $12.92 million for 2023. The exemption is gradually reduced for each donation above $16,000 per person per year in 2022 ($17,000 for 2023).

Tax Considerations When Selling Gifted Property

Anything left over would protect your estate from paying estate taxes at your death, provided the value of your estate is equal to or less than the remaining lifetime exemption. If you sell a gift you received, how it is handled depends on the market value of the gift and the profit you make, if any.

Source: s3.amazonaws.com

Source: s3.amazonaws.com

Suppose your grandmother is a famous artist and gives you a painting worth $1 million. You turn around and sell it for $500,000. The IRS believes that you would be giving the buyer a gift worth $500,000 since your grandmother's artwork was valued at $1 million.

That's $485,000 more than your $15,000 annual exclusion, so you'll need to subtract $485,000 from your lifetime exclusion. If you decide to sell the gift for fair market value, you must report a capital gain or loss, and you may have to pay capital gains tax if you make a profit.

Capital gains or losses on donated property acquired during the donor's lifetime are calculated based on the owner's original cost of the property. However, its cost base would be "stepped up" to its value at the date of his death if you inherited the property instead, i.e.

Gifts Are Not Income

j. if the original owner decided to wait to transfer it to you until his death. It can make a big difference. The donation basis is what the original owner paid for the property plus minus any adjustments. Typical adjustments that increase basis are substantial repairs and improvements and any expenses associated with the sale, such as brokerage commissions.

Typical adjustments that reduce basis include depreciation that the previous owner may have claimed on the rental property. These depreciations also pass to the new owner. The recipient's gain or loss on the gift would be the sales price minus this adjusted cost basis. Let's say one of your relatives transfers their $300,000 home to you before they die.

Source: image1.slideserve.com

Source: image1.slideserve.com

They paid $80,000 for it 30 years ago and have made $40,000 worth of improvements over the years. So your cost basis is $120,000 ($80,000 plus $40,000). If you sold the house for $300,000, you would have a capital gain of $180,000. Now let's assume that your relative transfers their house to you as part of their estate plan upon their death.

As a result of this basic increase, the situation is very different. If the fair market value of the property at the date of death is $300,000 and you sell it for $300,000, there is no capital gain to be taxed. In either case, you'll get $300,000, but in the second scenario, you won't have to give anything to the IRS.

The Annual Exclusion And The Lifetime Exemption

The recipient of the gift is also given the donor's tenure in the property to determine whether the gain is long-term or short-term. This is a short-term gain if the donor holds the property for a year or less. It is a long-term gain if they hold the asset for more than a year.

The inheritance will be taxed at the long-term capital gains rate on sale, regardless of how long the donor held. This holding period is an important distinction because it determines the rate at which your capital gain is taxed. The short-term gain is taxed as ordinary income depending on your tax bracket.

For tax years 2022 and 2023, regular federal tax rates range from 0% to 37%. The long-term gains rate is 0%, 15% and 20% for 2022 and 2023, depending on your taxable income. Most people fall into the 15% category. Long-term gains are more tax efficient than short-term gains.

Source: d20ohkaloyme4g.cloudfront.net

Source: d20ohkaloyme4g.cloudfront.net

Let's say you're single and earn $80,000 in tax year 2023. You'd pay 15% long-term capital gains tax, but you'd pay 22% on every dollar in the group. 22% tax if the profit is short-term. and you were taxed according to your tax bracket. This is a significant difference of 7%.

Selling A Gift Below Market Value

The income limits that apply to each tax rate can change each year because they are adjusted for inflation. Ask the donor to provide you with the base price of the property and the date it was originally purchased. Try to get a copy of the escrow statement or other documentation to prove the amount and date of purchase.

You'll also want to get an estimate of the property's fair market value on the date of the gift, as market value can sometimes come into play in the gain or loss calculations. This estimate can be as simple as getting a real estate appraisal done.

Consider living in the home for at least two to five years before selling it if you receive the property as a gift. This residency period can help you qualify for a capital gains exclusion of up to $250,000 on the sale of your principal residence if you're single, or $500,000 if you're married filing jointly.

Other rules also apply. To calculate capital gains tax on the sale of donated property, you must first determine the basis of the donated property. To calculate the gain, you take the donor's adjusted basis just before the gift is received. You will then increase or decrease the basis for any necessary adjustments from the time you own the property.

fmv of gifted property, cost adjusted basis for donations, donor's adjusted basis of gift form 709, gift cost basis rules, cost basis for gifted house, determining cost basis of inherited property, basis in gifted property, irs gift tax guide