Canada Gift Tax

Canada Gift Tax - With the end of the annual giving season and the start of tax season, it's time to review the cross-border tax implications for Canadians. Affected customers include US citizens and green card holders living in Canada, snowbirds who own property in the US, and Canadians planning to move to the US.

Source: www.canada.ca

Source: www.canada.ca

Canada Gift Tax

Because the CRA and the IRS have different approaches to gift taxes, clients may not be aware that they are subject to the US transfer tax system, which includes gift tax, estate tax, and transfer tax. This article will focus only on gift taxes. Let's start with a brief overview of Canada.

As far as Canadian advisors know, there is no gift tax in Canada. With the exception of gifts from employers, acts of donation are not taxable to either the donor (the donor) or the recipient (the donee). But that doesn't mean it's tax-free. Since the transfer of ownership of fixed assets is considered a disposition for Canadian tax purposes, gifts of fixed assets have tax consequences, unlike gifts of cash.

In Canada, if a father gives his son an asset that has a market value of $500,000 or a value of $300,000 at the time of the gift, the father is subject to an unrealized capital gains tax of $200,000. The interest will then purchase the property for a market value of $500,000.

Canadian Tax Treatment Of Gifts

Before diving into the complexities of US gift tax, it's important to understand that Canadians planning to move to the US should consider making future gifts before leaving Canada. This (and depending on the client, the trust may be optimal) has two main advantages: Unlike Canada, the US imposes a gift tax.

Source: www.personalfinancefreedom.com

Source: www.personalfinancefreedom.com

The tax is levied on the donor, not the recipient. In addition to all US residents, advisors should be aware that the United States is subject to a gift tax: Gift taxes range from 18% to 40%. There is an annual exemption and a lifetime exemption, but Canadians are only eligible for the annual exemption.

Annual Exclusion (applicable to US citizens, residents and Canadian citizens donating real estate in the US) Donors can deduct the first $15,000 (as of 2019) of annual gifts per recipient without limit to the total number of recipients. For example, a family with three children can both give $15,000 to each of their three children in 2019.

You can also make unlimited gifts to your US citizen spouse without tax implications. Gifts to non-U.S. spouses qualify for a $155,000 special deduction (as of 2019). Gifts that exceed the $15,000 or $155,000 annual threshold are taxable and must be reported on a gift tax return (IRS Form 709).

Canadian Tax Treatment Of Gifts

To qualify for these exceptions, the gift must have a "present interest," meaning that the donor has a right to the immediate use and enjoyment of the property received. In addition to the annual exemption, US citizens and residents may also claim a lifetime gift tax exemption.

This is a tax deduction for lifetime gifts of up to $11.4 million (as of 2019). It's called the "pooled credit" because it combines the estate tax exemption for US citizens and residents: any taxable gifts made during life are exempt from estate tax upon death.

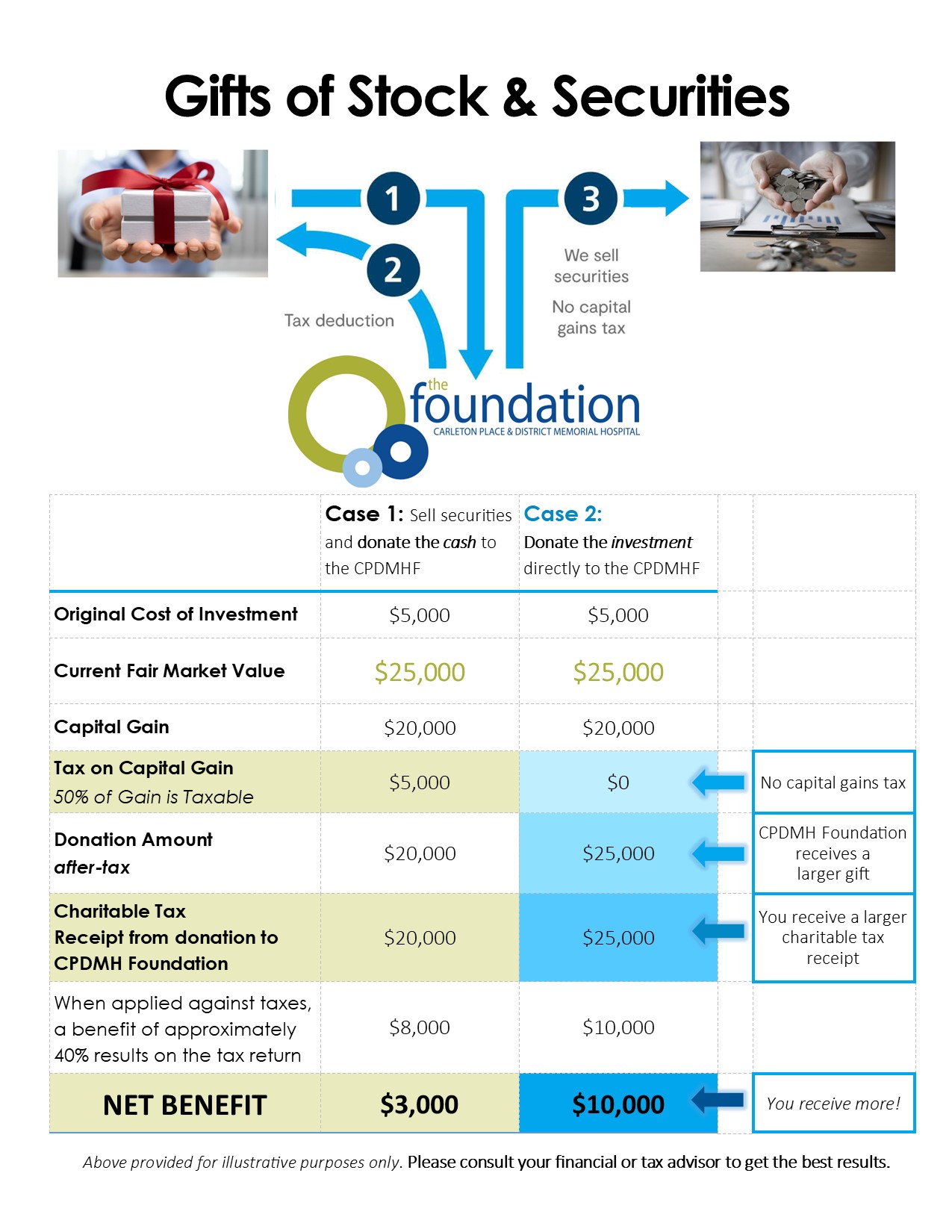

Source: www.carletonplacehospital.ca

Source: www.carletonplacehospital.ca

Canadians gifting property to the United States are eligible for the $15,000 and $155,000 annual exemptions, but are not exempt from the lifetime gift tax, so Canadians gifting assets above these thresholds must file a U.S. tax return and pay the gift tax. This leads to two cross-border tax traps for snowbirds donating US property.

There is a workaround for the first error, but not the second. Let's go back to the first example of a father transferring property to his son. This time we will make them American. There is no capital gains tax because the US is gift taxed (although not taxed) and does not treat gifts from father to son as character as Canada does.

Planning Opportunity For Canadians Moving To The U.s.: Pre-Exit Gifting

America simply shifts the father's cost base to the son. Using the same numbers as above, this means that the entire $200,000 unrealized capital gain will be taxable when the interest is finally disposed of. Differences in the timing of gifts of capital assets in Canada and the United States create the potential for double taxation if a Canadian donates assets located in the United States.

In Canada, the unrealized value of the gift is subject to capital gains tax on the father, but not in the US. By recognizing them at different times, foreign tax credits in both countries may not fully offset the tax and may result in double taxation.

Fortunately, relief from this capital gains double taxation problem is available through a treaty that allows the donor to elect accelerated US capital gains taxation in Canada. These circles are recognized in the US when donating. This coincides with the income tax period of the two countries and allows taxpayers to take advantage of foreign tax credits to eliminate double taxation.

Source: i.ytimg.com

Source: i.ytimg.com

Second tax pitfall: Canadians whose assets are subject to US gift tax are still double-taxed because the US gift tax and Canadian capital gains tax were introduced in the same year. (For example, our Canadian father and son would be taxed twice if they gifted property to the US.) This agreement would provide a US estate tax credit for the Canadian capital gains tax paid upon death, but no gift tax credit.

Planning Opportunity For Canadians Moving To The U.s.: Pre-Exit Gifting

In the US versus Canadian capital gains tax on lifetime gifts. The result is double taxation. Cross-border tax planning is important to minimize US gift tax issues for Canadians. For Canadians planning to move to the United States, there is a major gift planning opportunity before departure.

There are also planning solutions for snowbirds with US estates to avoid US probate without incurring US gift tax. It is important to seek professional advice abroad to deal with the complex tax interactions between Canada and the United States. Jonah Ravel, B.A., F.Pl., CFP is a Senior Cross Border Financial Planner at MCA Cross Border Advisors Inc.

These instruments preserve capital, offer stable income and protect against volatility. The NEI Clean Infrastructure Fund expands NEI's portfolio of investment funds to help investors drive the "big global transition" to clean electricity infrastructure. In this series of videos and articles, TD Wealth professionals share practical strategies that have helped them build successful careers.

NBFWM offers a wide range of services and security for its customers, with the infrastructure of a bank, but with the sensibility of a name. The CRA says that digitally filed tax returns will be processed automatically "without delay" as part of legislative changes to RESPs and RDSPs, as well as allowing for increased CDIC limits, with the agency saying that all paper returns will be "reserved for future processing."

canada gift tax limit, how much is the gift tax, canada tax gift from parent, federal gift tax exemption, gift from parents taxable canada, tax free gifts to adult children, us canada gift tax treaty, gift tax calculator